What Is Investor Matchmaking? A Guide for Startup Conference Organisers

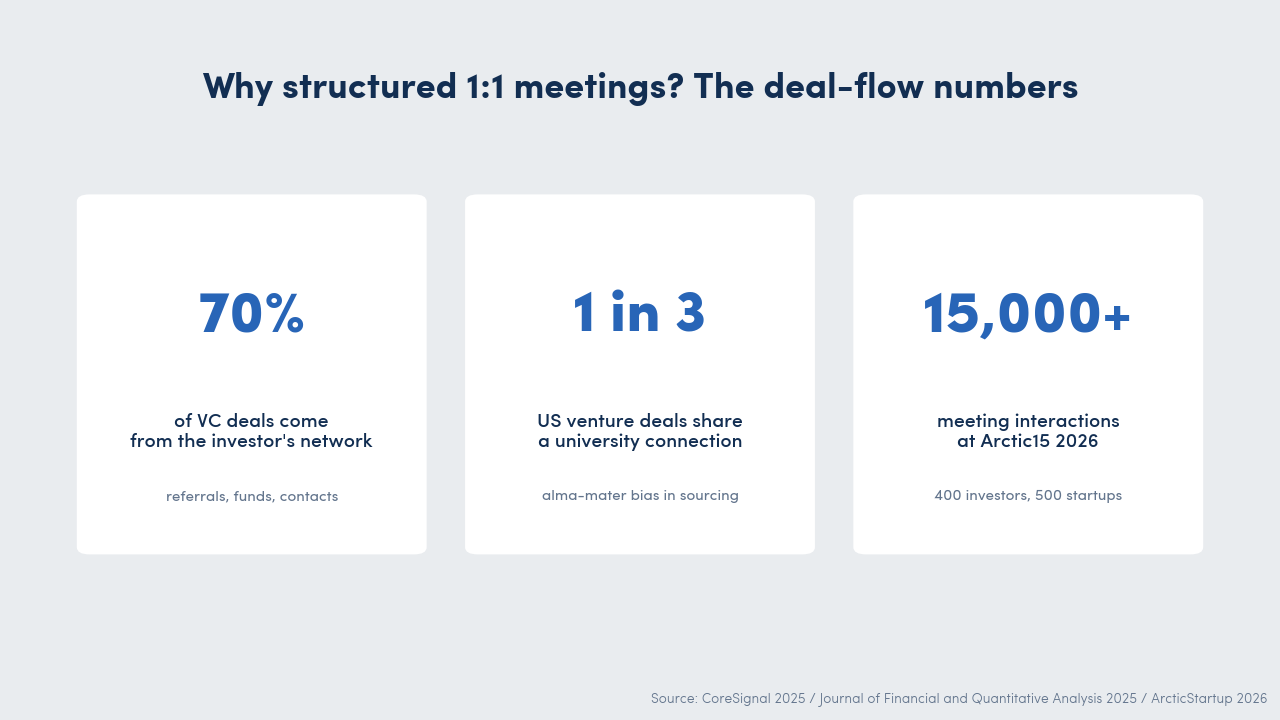

In June 2026, Arctic15 in Helsinki put 400 investors and 500 startups in the same building for two days. The outcome was more than 15,000 meeting interactions, roughly six meetings per attendee per day. Nobody found those meetings by luck at a coffee station. Every single one was requested, accepted and scheduled before the doors opened.

The system behind that has a name. Investor matchmaking is the structured process of pairing startup founders with relevant investors at an event, based on investment thesis, funding stage, sector and traction data. Instead of leaving contact to chance, organisers use profile data and matching rules to pre-schedule one-to-one meetings that both sides have accepted.

This guide explains investor matchmaking from the organiser’s side of the table: what data it needs, how the matching logic works, how it differs from a demo day or a pitch competition, and how you measure whether it delivered.

The short version: Investor matchmaking replaces chance encounters with pre-scheduled 1:1 meetings between founders and investors. It runs on three layers: profile data, matching logic and meeting logistics. Research shows around 70 per cent of venture deals come from the investor’s existing network, and that network is measurably biased. Structured matchmaking widens access, keeps top investors from being flooded, and gives you a measurable meeting programme instead of a hopeful coffee break.

What is investor matchmaking?

Investor matchmaking is a service the event provides, not an app feature founders stumble into. As the organiser, you collect structured profiles from both sides, define who should meet whom, and turn those decisions into a schedule of confirmed meetings. The meeting is the product. Everything else supports it.

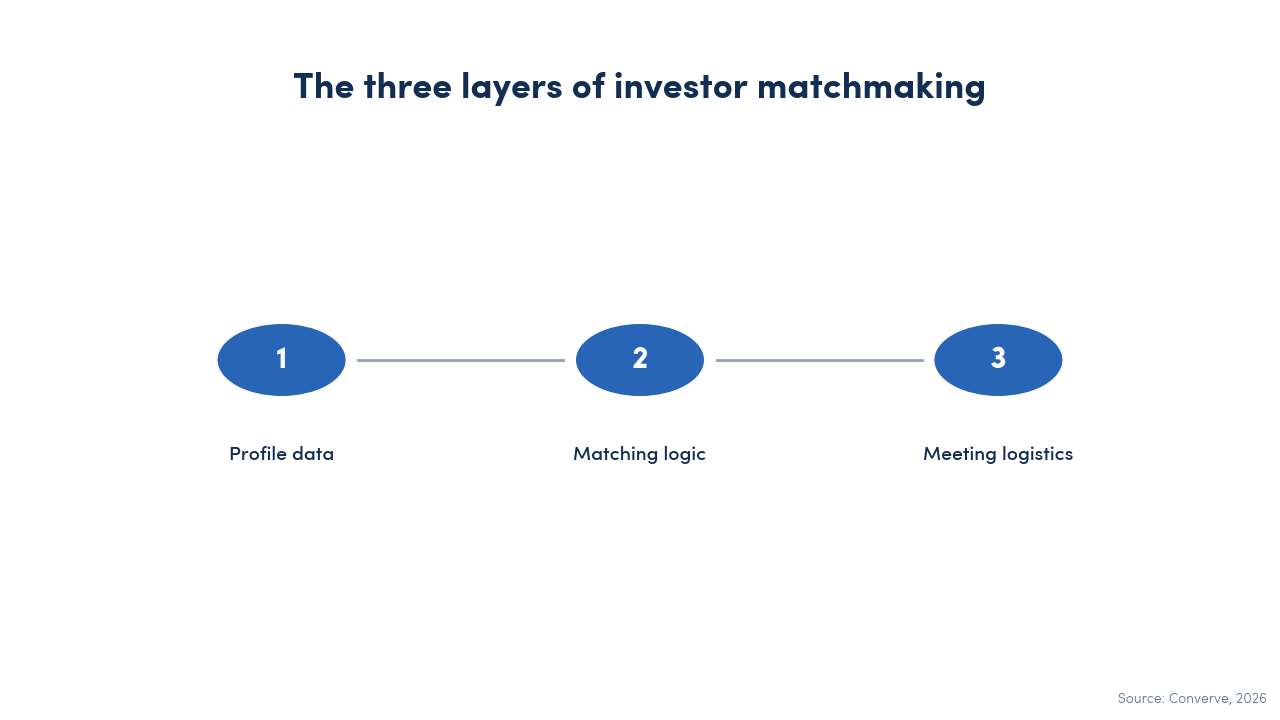

The process runs on three layers:

- Profile data: investors declare their thesis, stage, sector and ticket size. Startups declare their round, traction, sector and what they need beyond money.

- Matching logic: rules or scores decide which pairings make sense, and both sides confirm through a request and accept workflow.

- Meeting logistics: the platform assigns time slots and tables, handles reschedules and no-shows, and records what actually happened.

A few related terms are worth separating. Investor speed dating is a compressed format of the same idea, usually with fixed 10-minute rotations. Office hours are investor-hosted slots that founders book without curation. Reverse pitching flips the stage: investors present their thesis to founders. All three can sit inside a matchmaking programme, but none of them replaces the data and logic layers that make the meetings relevant. For the broader distinction between open networking and structured meetings, see our guide on event networking vs matchmaking.

Why do startup conferences need structured 1:1 meetings?

Because the informal alternative is already structured, just not by you. Research on venture capital (VC) deal flow shows that roughly 70 per cent of deals come from connections inside the investor’s existing ecosystem: portfolio referrals, fund networks and personal contacts (CoreSignal, 2025). A 2025 study in the Journal of Financial and Quantitative Analysis found that one third of US venture deals involve a founder and an investor from the same university.

That network effect has a cost. When VC firms gain new alumni connections, investments in alumni startups rise by about 8 per cent, but those deals show 23 per cent higher failure rates and far lower IPO (initial public offering) rates (Huang, 2023). Similar work on shared ethnicity points the same way: informal networks match people by similarity, not by fit, and outcomes suffer (Bengtsson and Hsu, Journal of Business Venturing, 2015).

For you as an organiser, this research is the business case. If deals follow networks, and networks are biased, then a conference that only offers open networking reproduces the bias. Structured matchmaking gives a first-time founder from an unknown university the same route to a relevant investor as a warm introduction gives an insider. It also protects the other side: investors get a curated schedule instead of a hundred cold pitches in a hallway. If investor overload is your specific problem, we have written a dedicated playbook on preventing investor overload at demo days.

The market has moved this way for a reason. Slush reported more than 20,000 pre-booked 1:1 meetings through its event app in 2025. Startup Grind ran over 800 pre-scheduled founder and investor meetings at its 2026 conference. Web Summit hosted a record 1,857 investors in 2025, up 74 per cent year on year. Meeting volume has become the metric conferences compete on, because it is the number founders and investors actually buy tickets for.

How investor matchmaking works: the three layers

The three layers from the definition deserve a closer look, because each one contains the decisions that determine whether your meetings are relevant or merely numerous.

Layer 1: profile data

Matching quality is capped by data quality. From investors, collect the investment thesis in structured form: stages (pre-seed to Series B, for example), sectors, geographies, ticket size and how many meetings they want per day. From startups, collect the current round, amount raised so far, sector, traction numbers and the team’s location. Keep the forms short. Ten well-chosen fields beat forty optional ones, because completion rates drive match rates. Collect this data at registration, not two days before the event, so your team has time to review the outliers.

Layer 2: matching logic

This is where organisers face a real choice. The default that has run trade shows for decades is a rule-based meeting matrix: you define which participant groups can meet (investors and startups, yes; startups and startups, optional), apply hard filters such as stage and sector fit, and let both sides browse, request and accept within those boundaries. The logic is transparent. When an investor asks why they were shown a fintech startup, you can answer, because every rule is visible and auditable.

Artificial intelligence scoring can sit on top: it ranks suggestions by predicted fit using behaviour and profile signals. That can lift relevance at large events, but it trades away explainability, since neither you nor the investor can fully reconstruct why the algorithm ranked one founder above another. Our advice is pragmatic: run a transparent rule layer as the foundation, and treat AI ranking as an optional enhancement, not the black box your whole programme depends on. How you weight founder quality against investor preferences is its own craft; our playbook on matching founders with the right VCs covers it step by step.

Layer 3: meeting logistics

The last layer turns accepted matches into meetings that actually happen. Fix slot lengths between 15 and 30 minutes for first conversations. Assign numbered tables in a dedicated meeting area, away from the stage noise. Build in buffer slots for reschedules, and send reminders 24 hours and 15 minutes before each meeting. Well-run programmes keep no-show rates under 20 per cent and hold kept-meeting rates around 80 per cent. The mechanics of squeezing the most meetings out of a two-day agenda are covered in our guide on maximising investor meetings at a 2-day conference.

Investor matchmaking vs. demo day vs. pitch competition vs. open networking

These formats are often mixed up because they share a goal: connecting founders with capital. They differ in structure, output and what you can measure afterwards.

| Format | Structure | Typical output | Success metric |

|---|---|---|---|

| Investor matchmaking | Pre-scheduled 1:1 meetings based on profiles and rules | Confirmed, relevant conversations | Kept meetings, follow-up rate |

| Demo day | Curated cohort pitches on stage to an invited audience | Visibility for a batch, inbound interest | Investor follow-ups per startup |

| Pitch competition | Startups compete for a prize before a jury | A winner, press attention | Applications, audience, coverage |

| Open networking | Unstructured mingling, receptions, coffee breaks | Chance encounters | Hard to measure |

The formats combine well. A strong startup conference often runs a demo day on stage while the matchmaking programme fills the tables next door. If you are new to the stage format, start with our organiser’s guide to what a demo day is. The point is not to pick one format, but to know which outcome each one is built to produce.

How do you measure whether it worked?

Matchmaking is the most measurable thing you will run at your event. Four numbers tell you most of the story:

- Match acceptance rate: the share of meeting requests that get accepted. 40 to 60 per cent is a healthy range; below that, your matching logic or your data is off.

- Kept-meeting rate: the share of scheduled meetings that actually happen. Aim for 80 per cent or better.

- Meetings per investor: shows whether your supply side got value. Compare it against the number they asked for.

- 14-day follow-up rate: the share of meetings that led to a second conversation. This is the number that predicts whether investors return next year.

Collect the first three from your platform automatically, and the fourth with a short survey two weeks after the event. Report all four to sponsors and investors. A conference that can say “82 per cent of 1,200 scheduled meetings took place, and a third produced follow-ups” has a renewal argument no stage programme can match.

Solution: matchmaking investors can trust

Solution: Converve runs investor matchmaking on a rule-based meeting matrix. You define which groups meet, which filters apply and how slots are allocated, and every matching decision stays visible and auditable. AI-assisted suggestions are available where they help, without turning your programme into a black box. Profiles, requests and meeting data stay GDPR (General Data Protection Regulation) compliant, which matters when your attendee list is full of funds and their portfolio data. Conference teams use Converve to run exactly the kind of programme this article describes, from profile forms to the post-event meeting report.

Conclusion

Investor matchmaking is the organiser’s answer to an uncomfortable fact: deals follow networks, and networks are biased. By collecting structured profiles, matching on declared fit and scheduling confirmed 1:1 meetings, you turn the most valuable part of your conference from an accident into a programme. Start with clean profile data, keep the matching logic transparent, run the logistics tightly, and measure the four numbers that matter. Your founders get access on merit. Your investors get a schedule worth the flight. And you get a metric that sells next year’s tickets.

Want to see how a meeting matrix would look for your event? Talk to us and we will walk you through a live setup.

Frequently asked questions

What is the difference between investor matchmaking and a demo day?

A demo day is a stage format: a curated cohort of startups pitches to an invited audience, and interest flows in afterwards. Investor matchmaking is a meeting format: founders and investors are paired through profiles and rules, and every conversation is scheduled before it happens. Many conferences run both, using the stage for visibility and the matchmaking programme for confirmed 1:1 meetings.

What data does investor matchmaking need?

From investors: investment thesis, preferred stages, sectors, geography, ticket size and meeting capacity per day. From startups: current round, traction, sector, location and what they seek beyond capital. Ten mandatory, well-designed fields outperform long optional forms, because completion drives match quality.

How many investor meetings fit into one conference day?

With 15 to 30 minute slots, breaks and a lunch window, eight to twelve meetings per investor per day is a realistic ceiling. Arctic15 averages about six meetings per attendee per day across its whole programme. Ask each investor for their limit during registration and schedule below it, since a tired investor is a poor meeting partner.

Does investor matchmaking need artificial intelligence?

No. The foundation is a rule-based meeting matrix: defined groups, hard filters and a request and accept workflow. That alone produces relevant, auditable schedules. AI scoring can improve suggestion ranking at large events, but it is an optional layer, and it should never make decisions you cannot explain to an investor afterwards.

How do you measure the success of investor matchmaking?

Track four numbers: match acceptance rate (40 to 60 per cent is healthy), kept-meeting rate (aim for 80 per cent), meetings per investor against their requested capacity, and the 14-day follow-up rate. Together they show whether meetings were relevant, whether they happened, and whether they led anywhere.