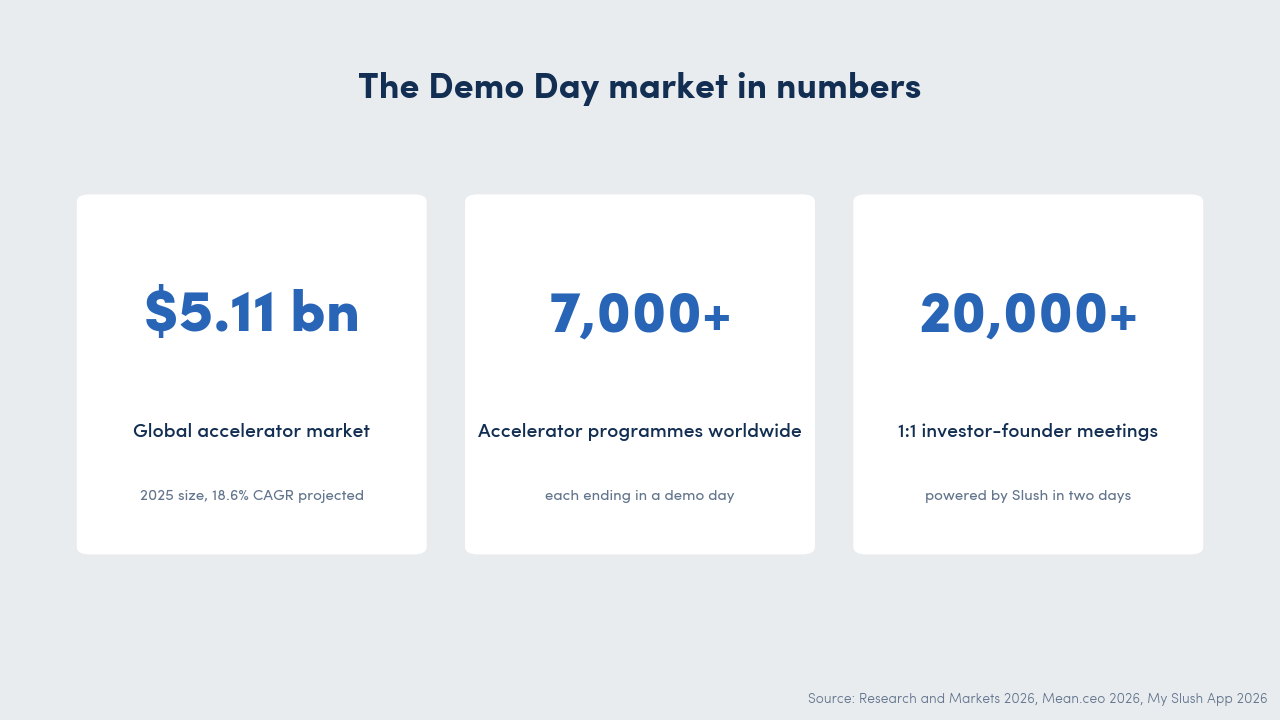

What is a Demo Day? A Complete Guide for Startup Conference Organisers

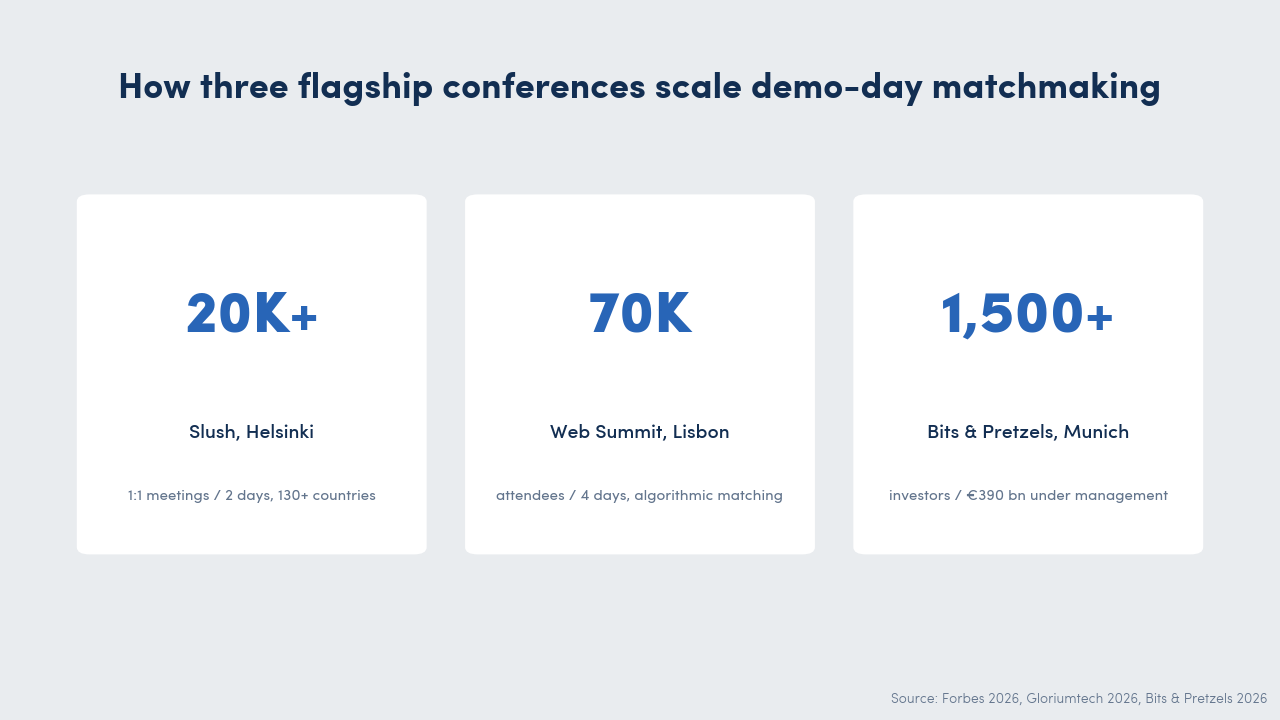

Slush powers more than 20,000 one-to-one investor-founder meetings in two days. Y Combinator funnels 250 startups onto a single stage four times a year. Bits & Pretzels brings 1,500-plus investors with €390 bn in assets under management into one Munich hall. None of those numbers happen by accident. They happen because someone designed the demo day around investor follow-ups, not pitch slots.

If you are planning a demo day for the first time, or rebuilding one that is producing lots of applause and few signed term sheets, this guide is for you. We walk through what a demo day actually is, the four formats organisers should know, how a demo day differs from a pitch event or a networking event, how three of Europe’s largest startup conferences structure their matchmaking, and the five things organisers must get right to turn pitches into follow-ups.

What is a Demo Day?

A demo day is a structured event at which startups from an accelerator, incubator, or venture programme pitch their business to a curated audience of investors, corporate partners, and press. Each company gets five to ten minutes on stage, followed by a short Q&A and a window of one-to-one investor meetings.

The phrase was popularised by Y Combinator (YC), which has run a cohort demo day at the end of each batch since 2005. Today, more than 7,000 accelerator and incubator programmes worldwide end with some version of the same event. The format has become the de facto graduation ritual of the early-stage startup world.

What the format does for founders is obvious: it concentrates investor attention. What it does for organisers is less obvious but more interesting: it forces every weakness in the programme to surface in a single afternoon. A weak cohort cannot hide. A poorly curated investor room cannot hide. An under-designed follow-up process cannot hide. The demo day is, in effect, a stress test of the entire programme.

The Four Demo Day Formats (and How They Differ)

Demo days fall into four recurring formats. Knowing which one you are running shapes every other decision, from the room size to the matchmaking software.

- Accelerator demo day: The classic format. A cohort of 10 to 300 startups graduates from a three- to four-month programme and pitches on a single day. YC, Techstars, and 500 Global are the household names. Investor curation is the host’s responsibility, and the pitch order is usually rehearsed for narrative tension.

- VC-firm demo day: A venture firm runs its own studio or generator cohort, then hosts an investor stream for co-investors. Antler is the model. Cohorts are smaller (often six to twelve teams), the room is more intimate, and the lead investor is also the host. This shifts the dynamic from competitive pitching to syndicate-building.

- Conference demo day: A pitch stage embedded inside a larger startup conference. Slush has its investor-only matchmaking stream, Web Summit runs PITCH, and Bits & Pretzels reserves an investor stage inside its Munich festival. The pitch slot is one signal among many, and most of the actual deal motion happens in the matchmaking app, not on the stage.

- Standalone demo day: University or ecosystem-driven events, often regional. Aalto Startup Center in Helsinki, StartX at Stanford, and city-led innovation hubs are examples. These tend to combine a pitch competition with an exhibition floor and depend on local investor networks for impact.

If you are unsure which format applies to you, start with the cohort. A defined batch with a graduation date implies an accelerator or VC-firm demo day. A general invitation with a curated pitch line-up inside a wider event implies a conference demo day. A regional showcase without a multi-week programme behind it is a standalone format.

Demo Day vs. Pitch Event vs. Networking Event

The three terms get used interchangeably, especially in marketing copy. They should not be.

| Format | Cohort behind it | Audience | Structure | Primary outcome |

|---|---|---|---|---|

| Demo day | Yes (3- to 6-month programme) | Curated investors and partners | Time-capped pitches plus Q&A, then 1:1 window | Investor follow-ups |

| Pitch event | Optional | Open or semi-curated | Pitch competition with judges and prizes | Visibility plus prize money |

| Networking event | No | Open | Free-form mingling | Relationship-building |

A demo day is built on the back of a programme. A pitch event is built on the back of a competition. A networking event is built on the back of a room. The downstream consequences are large. A demo day investor expects to see a vetted cohort. A pitch-event judge expects to see a winner emerge. A networking-event attendee expects open conversation. Mislabel the event in your invitation, and your room shows up with the wrong expectations.

For a deeper comparison of how digital tools fit each format, our overview of the top event networking apps breaks tooling down by event type.

Who Attends a Demo Day — And Why Curation Matters More Than Headcount

The audience at a demo day is a carefully composed mix. Five groups recur.

- Venture capitalists (Series A and growth funds for later-stage demo days, seed funds for earlier-stage cohorts): the headline audience. The number you actually care about is not how many show up, but how many partners with cheque-writing authority show up.

- Angel investors and family offices: typically write smaller cheques but move faster than institutional funds. They matter more in early-stage and regional demo days than at scaled conference formats.

- Corporate development teams: strategic investors and acquirers. Their interest is rarely the next round; it is the next partnership or the next acquisition. They want to meet founders, not pitch back at them.

- Press and industry analysts: demo days are media moments. A startup that lands a TechCrunch write-up post-demo-day raises a different round than one that does not.

- Limited Partners (LPs) and ecosystem stakeholders: the supporting cast for accelerator and VC-firm demo days. They are watching the programme as much as the startups.

The mistake that ruins demo days is mistaking headcount for curation. A room of 600 names with 12 decision-makers is worse than a room of 80 names with 60 decision-makers. The latter generates follow-ups. The former generates LinkedIn requests.

This is also where sponsorship strategy enters the picture. If your demo day has sponsors, they should be selected for fit with the cohort, not for cheque size. Our guide on virtual event sponsorship packages covers how to structure tiered offers when sponsors and investors overlap.

How Three Leading Conferences Structure Demo-Day Matchmaking

The largest startup conferences in Europe have made demo-day matchmaking a core part of their product. Their approaches differ, and the differences are instructive.

Slush, Helsinki (18 to 19 November 2026). The Finnish flagship hosts 12,000 to 20,000 attendees from more than 130 countries. The “My Slush” app, built on a dedicated meeting tool, powers more than 20,000 pre-booked one-to-one meetings in two days. Slush curates participants on both sides of the marketplace and uses a request-and-accept model, which keeps quality higher than a free-for-all calendar. Founders apply for the investor stream; investors confirm meetings the founders propose.

Web Summit, Lisbon (9 to 12 November 2026). The largest of the three by headcount, with more than 70,000 attendees. Web Summit operates what Forbes called “genuinely good, probably the best among large conferences” for matchmaking in its 2026 review. The platform scales differently than Slush: with so many participants, Web Summit leans on algorithmic suggestions and curated side events to keep matchmaking from drowning under volume.

Bits & Pretzels, Munich (28 to 30 September 2026). Smaller and deliberately Bavarian. 7,500 attendees, 1,500-plus investors with €390 bn under management. The event combines pre-scheduled matchmaking with an Oktoberfest table-share model. Founders and investors literally end up at the same wooden bench. The format works because the informality lowers the access bar to investors who would never accept a cold LinkedIn request.

The pattern across all three is consistent. The pitch stage is the headline; the matchmaking platform is the engine. Organisers who only buy the headline get applause. Organisers who buy the engine get follow-ups.

Five Things Organisers Must Get Right

Most demo-day failures are not about the cohort or the venue. They are about five operational choices that the audience never sees.

1. Curate Investors by Thesis-Fit, Stage-Fit, Geo-Fit

Filter your investor list against three criteria before sending any invitation. Thesis-fit means the fund actually invests in the sectors represented in your cohort. Stage-fit means the cheque size matches the round you are signalling. Geo-fit means the fund operates in your cohort’s market, or has a partner who does. A Series A fund attending a pre-seed demo day is a wasted seat. So is a US-only fund at a programme with only European companies.

The result is not a smaller room. It is the same-size room with three times the conversion rate.

2. Cap Pitch Time and Build Q&A Into the Schedule

Five to ten minutes per pitch is the working standard, with three to five minutes of Q&A. Cap it hard. Audiences can absorb four high-quality pitches per hour; they cannot absorb seven. Build the Q&A into the published agenda, not as an afterthought. Investors form their views in the Q&A, not in the pitch. The Q&A is what tells you whether the founder can think on their feet.

3. Open a 1:1 Meeting Window Directly After the Pitches

This is the single highest-leverage piece of operational design. The window between the last pitch and the end of the day is where deals start. Most demo days waste it on a wine reception. The successful ones use a meeting platform to pre-schedule fifteen-minute slots in the immediate post-pitch hours, while attention is highest.

Solution: A B2B matchmaking platform like Converve lets investors and founders pre-book qualified one-to-one meetings, runs them as in-person or video slots, and produces a clean handover into your CRM (customer relationship management) system. For demo days with even modestly large cohorts, the alternative (manual coordination over email) costs the organiser more in lost meetings than the platform costs.

4. Build a Follow-up Hub for the First 14 Days

The demo day is not where deals close. The two weeks afterwards are. Build a follow-up hub with three things in it. First, a shared document for every founder containing investor introductions, the recording of their pitch, and a one-line “next step” prompt. Second, a structured warm-intro process: investors who flagged interest at the event should receive a follow-up within 48 hours. Third, a Mutual Action Plan template. Published research shows centralising post-demo materials this way lifted year-on-year win rates by 31 per cent in the B2B benchmark Dock and Nectar published in 2026.

5. Measure Demo Day From the Organiser’s Cockpit

Founders measure demo day by the round they raise. Organisers should measure four different things.

- Meetings per founder: the most important leading indicator. A cohort averaging fewer than eight pre-booked meetings per founder usually under-delivers on funding.

- Investor Net Promoter Score (NPS): ask attending investors a single post-event question. NPS below 30 means the curation was wrong. NPS above 50 means investors will come back.

- Fourteen-day follow-up rate: the share of founders who received a follow-up message from at least one investor within two weeks. Below 60 per cent is a warning.

- Ninety-day funding velocity: how many of the cohort have started or closed a round 90 days post-demo-day. Below 40 per cent in a Series-A-targeted demo day suggests stage-fit issues in the investor curation.

These four numbers tell you whether the demo day worked as a programme tool, not just as a stage.

Why Demo Day is a Starting Line, Not a Finish Line

The hardest truth in this category is that nine out of ten accelerator participants leave their programme without the funding they came in for. The demo day is not the cause. The follow-up is.

Research on European accelerators in 2026 puts it bluntly: founders who treat demo day as the finish line rather than the starting gun tend to leave disappointed. The number that actually predicts a successful round is not the size of the stage, the calibre of the audience, or the polish of the deck. It is the structured follow-up sequence in the two weeks that follow. Organisers who design for that sequence get cohort outcomes that justify the programme. Organisers who design only for the stage get applause.

This is also why the operational choices above matter more than the headline numbers. A demo day with 600 mid-tier investors in the room and no post-event follow-up structure produces less funding than a demo day with 80 fund decision-makers, a meeting platform, and a 14-day follow-up hub.

Frequently Asked Questions

What is a demo day in simple terms? A demo day is an event where startups from an accelerator or programme pitch their business to a curated audience of investors and partners, usually in five- to ten-minute slots, followed by one-to-one meetings.

How long is a typical demo day pitch? Five to ten minutes per company, plus three to five minutes of Q&A. Some VC-firm demo days run as short as three minutes per startup to fit more pitches into a single afternoon.

How does Y Combinator’s demo day work? YC runs four demo days per year, in March, June, September, and December, at the end of each batch. Each batch has 250 to 300 startups. The event is invitation-only for investors and lasts one to two days, with founders presenting in short slots and follow-up meetings booked through the YC investor portal.

What is the difference between a demo day and a pitch event? A demo day is the closing event of a defined programme and presents a vetted cohort. A pitch event is usually a competition with prizes, judges, and an open or semi-open line-up. Demo days are designed for follow-ups; pitch events are designed for winners.

Are demo days only for accelerators? No. The format has spread to VC firms, conference organisers, and university or government programmes. The common element is a defined cohort, a curated investor audience, and a time-capped pitch format.

How do organisers measure demo day success? From an organiser’s perspective, the four metrics that matter are meetings per founder, investor Net Promoter Score, fourteen-day follow-up rate, and ninety-day funding velocity. Founder funding alone is too narrow a metric to evaluate the programme.

Conclusion — Design the Follow-up, Not Just the Stage

A demo day is one of the most concentrated events in the startup calendar. For three to six hours, every weakness in the programme is on display, and so is every strength. The temptation is to invest in the stage: better AV, a bigger room, a longer guest list. The pay-off is in the operational layers behind the stage: investor curation, meeting platform, follow-up hub, and a measurement cockpit that tells you whether the cohort raised because of the demo day or in spite of it.

If you are planning your first demo day, or rebuilding one that is producing more applause than term sheets, start with the five operational levers above. They are the difference between an expensive Tuesday afternoon and a programme outcome that pays for itself.