Demo Day Structure: A Six-Phase Playbook for Maximum Investor Follow-ups

Most accelerator teams pour their energy into the pitch stage and treat the follow-up as housekeeping. That is the wrong order. The pitch is the headline, but the funding round is decided in the operational layers behind it: investor curation, pre-scheduled meetings, the warm-intro window, the 14-day follow-up hub. This playbook walks through the six phases that separate a demo day that produces follow-ups from one that produces applause.

Why follow-up structure decides demo day ROI

A demo day is one of the most concentrated outcome moments in a startup’s calendar. Industry data suggests that roughly 80 per cent of startups raise follow-on funding after participating in a structured demo day, but that figure hides huge variance. Cohorts with a deliberate post-event architecture consistently outperform those that leave investors to find their own way home. A B2B benchmark published by Dock and Nectar in 2026 showed that centralising follow-up materials (deck, recording, mutual action plan) lifted year-on-year win rates by 31 per cent in comparable sales contexts. The mechanism translates directly to investor follow-ups: the easier it is to revisit the pitch, the more often investors send a second email.

This is also why the headline numbers can mislead. A demo day with 600 mid-tier investors in the room and no post-event structure produces less funding than a demo day with 80 fund decision-makers, a meeting platform, and a follow-up hub. The composition of the audience and the friction of the post-event workflow predict outcomes more reliably than the size of the venue.

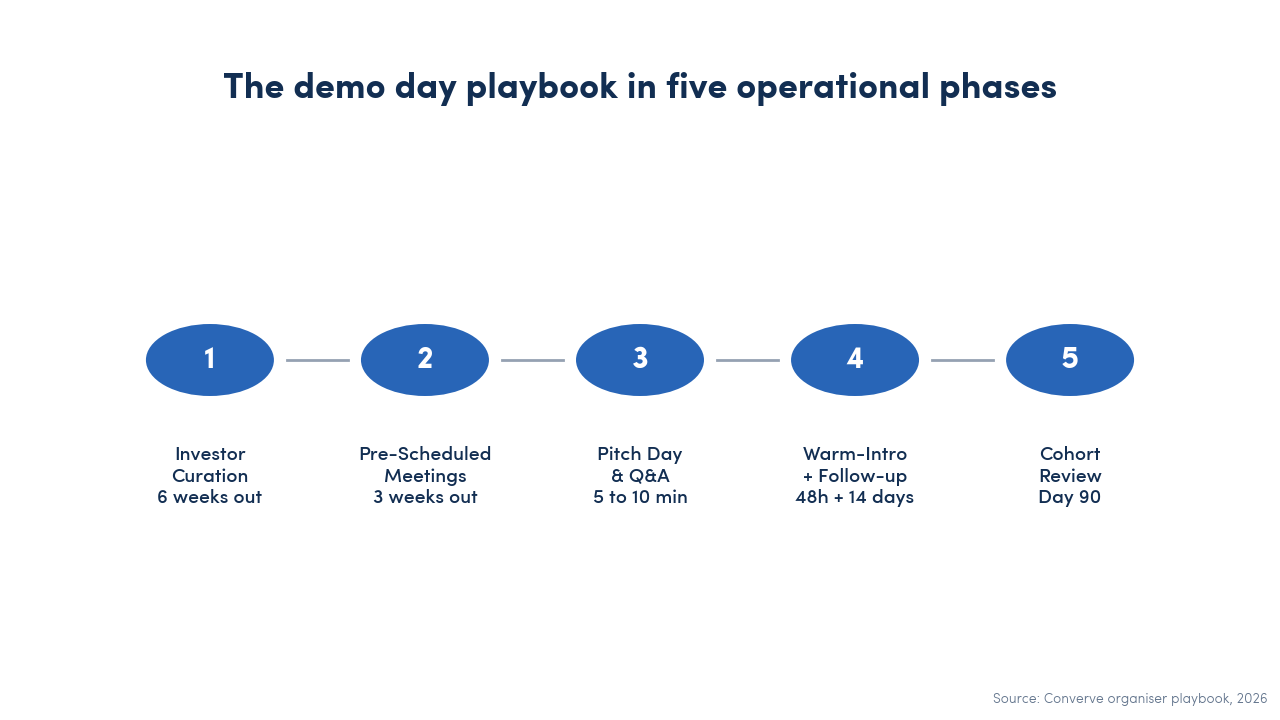

The Six-Phase Demo Day Playbook

The playbook below treats demo day not as a single event but as a six-phase programme that starts six weeks before pitch day and ends ninety days after. Each phase has a defined output, a clear owner, and a measurable handover to the next.

1. Investor Curation (Six Weeks Out)

Curation is where the funding round is actually built. Begin six weeks before pitch day with a written investor thesis for the cohort: stages represented, sector tilts, geographic constraints, ticket sizes likely to be relevant. Then build the invitation list from the bottom up against that thesis.

- Map the cohort first: list every startup with stage, sector, geography, current revenue, and the type of investor that would credibly lead their next round. Aggregate the totals. The invitation list should mirror the cohort, not the other way around.

- Favour decision-makers over volume: 80 partner-level investors with cheque-writing authority will produce more meetings than 600 associates collecting deal-flow lists. Track titles and last cheque size, not LinkedIn follower counts.

- Build a soft-commit pipeline: the new norm in 2026, as several Y Combinator alumni noted after the S25 batch, is to gather soft commits during the cohort weeks and only announce the round at demo day. Reflect that in your invitation cadence: warm investors two weeks before the event, not on the day.

2. Pre-Scheduled Meeting Architecture (Three Weeks Out)

The most reliable leading indicator of cohort funding is the number of pre-booked 1:1 meetings per founder. A cohort that averages fewer than eight meetings per founder almost always under-delivers on funding. Eight to fifteen is a healthy band; above twenty, the founders cannot follow up properly and quality drops.

- Open the matchmaking platform three weeks out: founders and investors flag mutual interest and book slots through a structured request flow. Avoid free-text email scheduling, it does not scale beyond fifty founders.

- Cap top-investor inboxes: the most active funds will receive every founder request. Set a maximum of fifteen meeting requests per investor profile and force founders to prioritise. This protects the top of the deal funnel and ensures founders who are less senior at a brand can still get in front of the right partners.

- Schedule against the published agenda, not against it: the 1:1 window should sit immediately after the pitch block, while attention is fresh. Booking meetings the next morning leaks half the investor energy.

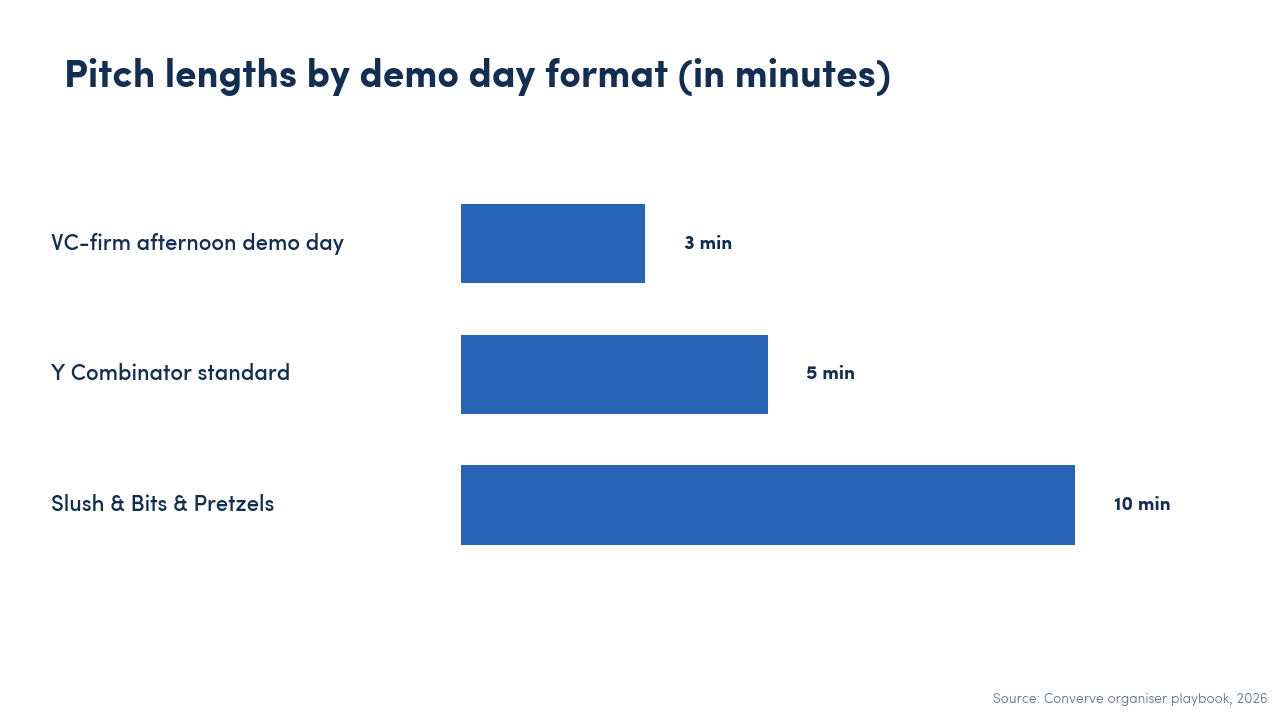

3. Pitch-Day Schedule and Q&A Discipline

The pitch day itself is the most visible phase, but its job is narrow: produce enough signal for investors to decide who they want to meet. Five to ten minutes per company is the working standard, with three to five minutes of Q&A. Some venture-firm demo days cap the pitch at three minutes to fit more founders into a single afternoon. The format you pick should match the cohort size: short pitches for large cohorts, longer pitches for showcase events.

- Cap pitch time, hard: audiences can absorb roughly four high-quality pitches per hour, not seven. Run a strict clock with a visible timer on stage. Founders who run over are interrupted, not extended.

- Build Q&A into the published agenda: investors form their judgement in the Q&A, not in the pitch. Three to five minutes per company is enough to surface whether the founder can think on their feet. Treat Q&A as a feature, not as the bit that gets cut when the schedule slips.

- Open the 1:1 window immediately after the last pitch: do not break for a long networking reception first. The friction of a context switch costs you meetings.

4. The 48-Hour Warm-Intro Window

The first forty-eight hours after a pitch are the warm-intro window, the period in which investor attention is sharp enough to convert a single follow-up message into a scheduled meeting. After that window closes, follow-up rates drop sharply. The lead-generation research is brutal on this point: in comparable B2B settings, leads contacted within five minutes convert at roughly nine times the rate of leads contacted later. Investor leads behave similarly, only on a slightly longer clock.

- Send a warm introduction within 48 hours: for every investor who flagged interest at the event, the organiser team writes a short, personalised intro email connecting them to the founder, with the recording link and one suggested next step.

- Triage by signal strength: not all expressions of interest are equal. Mark each interaction as cold, warm, or hot, and order the warm-intro queue by signal strength so the strongest threads are sent first.

- Avoid bulk introductions: a generic email to twenty investors with the cohort deck attached gets ignored. One-to-one warm intros, even if shorter, convert.

5. The 14-Day Follow-up Hub

The demo day is not where deals close. The fourteen days afterwards are. Build a shared follow-up hub containing three artefacts.

- A founder dashboard: per startup, the recording of their pitch, the investor list with status (cold, warm, hot, met, soft commit, term sheet), and a one-line next step prompt for every contact.

- A Mutual Action Plan template: a lightweight document that founders share with any investor who reaches the second meeting. It captures the next two steps, who owns each step, and the date the action closes. Investors with a written plan in front of them respond at roughly twice the rate of those without one.

- A central organiser inbox: founders forward investor follow-ups to a shared address tagged with the cohort. The organiser team monitors response patterns and steps in if a hot thread goes cold. Investors who flagged hot interest but have not received a follow-up within five days get a nudge from the organiser, not the founder.

6. Day-90 Cohort Review

Ninety days after pitch day, sit down with the cohort data and the investor data and answer one question: did the demo day cause the funding, or was it incidental to it? This is the only review that tells you whether the operational architecture worked.

- Run a closed-loop survey with investors: a single-question Net Promoter Score plus a free-text “what would you change”. Anything below NPS 30 means the curation was wrong; above 50 means the investors will come back.

- Run a closed-loop survey with founders: two questions. How many meetings did the demo day produce? How many of those meetings led to a second meeting? The ratio between the two is the single best diagnostic for the cohort.

- Publish a short cohort report internally: meetings per founder, fourteen-day follow-up rate, ninety-day funding velocity. Use it to brief the next cohort and recalibrate Phase 1.

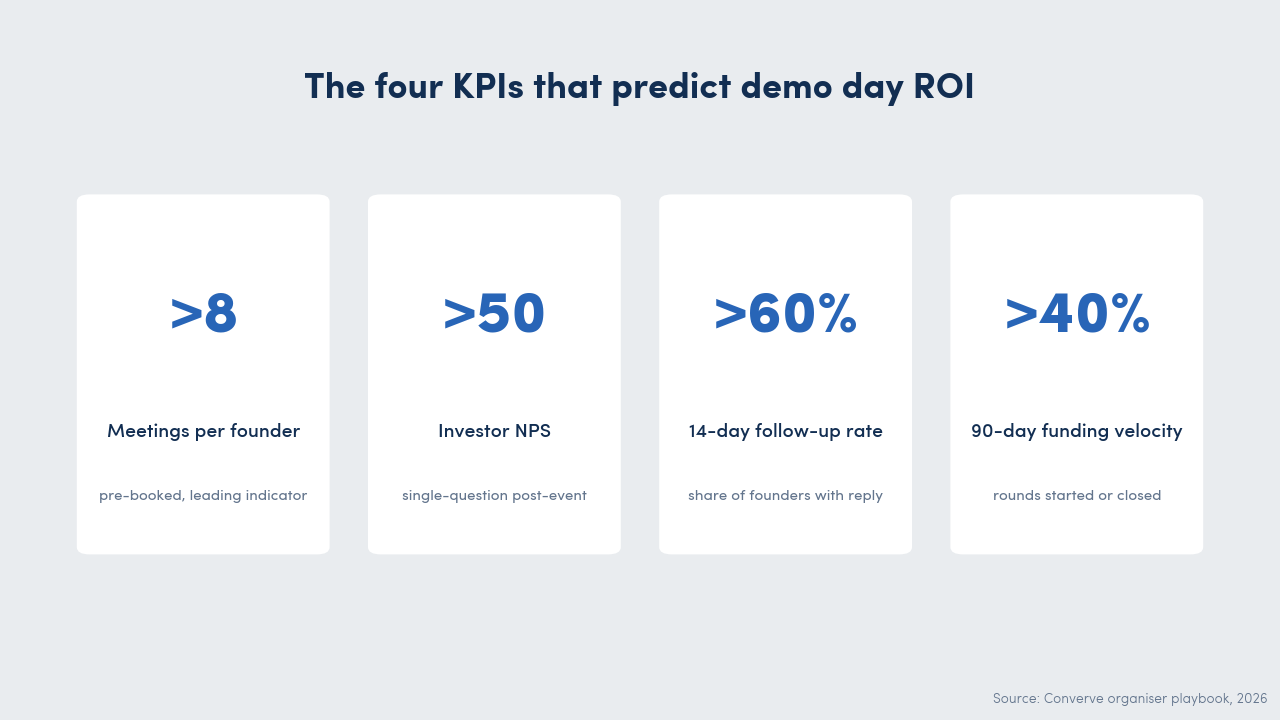

The Organiser KPI Cockpit

If you measure a demo day only by ticket sales and stage applause, you will optimise for the wrong things. The cockpit below contains the four metrics that consistently predict whether a cohort raises.

- Meetings per founder: the most important leading indicator. Below eight pre-booked meetings per founder, the cohort almost always under-performs. Eight to fifteen is the healthy band.

- Investor Net Promoter Score (NPS): ask attending investors a single post-event question. Below NPS 30, the curation was off-thesis. Above 50, the same investors come back next cohort.

- Fourteen-day follow-up rate: the share of founders who received at least one investor follow-up within two weeks. Below 60 per cent is a warning that the operational layer (introductions, hub, mutual action plans) is broken.

- Ninety-day funding velocity: the share of the cohort that has started or closed a round within ninety days of pitch day. Below 40 per cent on a Series-A-targeted demo day usually signals a stage-fit problem in the investor curation.

These four metrics, tracked cohort over cohort, will tell you more about programme health than any anecdote. If you read more about the underlying definitions, see our complete guide to demo days for organisers.

How Slush, Bits & Pretzels and YC Structure Their Demo Days

Three flagship formats illustrate how the playbook above plays out at scale, with different choices in each phase.

- Y Combinator: four batches per year, 250 to 300 startups per batch, two-day invitation-only format with very short five-minute pitches and a structured investor portal for follow-up booking. The cohort signs cohort-wide NDAs so investors see the same information at the same time, which compresses decision-making.

- Slush, Helsinki: a 25,000-attendee general conference rather than a closed accelerator demo day, but the matchmaking engine produces more than 20,000 pre-scheduled 1:1 meetings in two days across more than 130 countries. Pitch slots are longer (eight to ten minutes plus Q&A) and run on multiple stages in parallel; the centralised meeting platform replaces the curation function.

- Bits & Pretzels, Munich: 7,500 attendees with more than 1,500 investors representing €390 bn under management. The combination of pre-scheduled matchmaking and an informal Oktoberfest table-sharing model creates two parallel meeting channels. The informality lowers the bar to investors who would never accept a cold LinkedIn request.

The pattern across all three is consistent. The pitch stage is the headline; the matchmaking platform is the engine. Organisers who only buy the headline get applause. Organisers who buy the engine get follow-ups.

Five Common Mistakes Organisers Make

- Treating the pitch as the product: the pitch is signal, not deliverable. A great pitch with no follow-up architecture is a wasted hour.

- Inviting volume instead of decision-makers: 600 associates in the room sounds like a success metric. It is not. Eighty partners with cheque-writing authority outperform.

- Letting the matchmaking platform open too late: three weeks out is the working window. Opening it three days before pitch day produces unbalanced calendars and burned-out founders.

- No closed-loop survey: without an investor NPS and a founder ratio after ninety days, the next cohort starts from intuition rather than data.

- Treating Day 90 as the end: the cohort relationships are an asset. Founders who closed a round will reinvest in the programme as mentors; investors who came once and saw quality will come back. Plan the next cohort with the data, and the network compounds.

If you want a benchmark for what good matchmaking software looks like in this context, our overview of the best event networking apps for 2026 sets out the criteria that matter to demo-day organisers.

Solution: a single operating layer behind the stage

Most of the friction in the six-phase playbook comes from running it across five disconnected tools: a spreadsheet for the invitation list, a calendar tool for 1:1 bookings, an email client for warm intros, a shared document folder for the follow-up hub, and a survey tool for Day 90. Converve consolidates the operational layer into a single platform that combines investor curation, pre-scheduled matchmaking, an investor portal, and a follow-up hub with cohort analytics. That removes the seams where leads tend to fall through, and gives the organiser team one cockpit instead of five dashboards.

Conclusion

A demo day produces follow-ups when it is designed as a six-phase programme, not as a single event. Curation defines the funnel. Pre-scheduled meetings concentrate the signal. The pitch block creates the moment. The forty-eight-hour warm-intro window converts the signal. The fourteen-day hub turns conversion into momentum. The ninety-day review tells you whether the programme worked. Build the architecture once, measure the four KPIs cohort over cohort, and the next demo day starts from a stronger base than the last one.

If you want to discuss how Converve supports demo days at scale, from accelerator-batch formats to large-venue conferences, get in touch for a demo.

Frequently Asked Questions

How long should a demo day pitch be? Five to ten minutes per company is the working standard, with three to five minutes of Q&A. Some VC-firm demo days run as short as three minutes per startup to fit more pitches into a single afternoon. Cap the time hard and run a visible clock.

How many investors should we invite? Favour decision-makers over volume. Eighty partner-level investors with cheque-writing authority will produce more meetings than six hundred associates. Build the invitation list against a written cohort thesis, not against an open call.

How do you structure follow-up after a demo day? Treat the first forty-eight hours as the warm-intro window. Send personalised investor-to-founder intros within that window. Build a fourteen-day follow-up hub with a founder dashboard, a Mutual Action Plan template, and a central organiser inbox that catches hot threads going cold.

What KPIs should a demo day organiser track? Four metrics: meetings per founder (target above eight), investor NPS (target above 50), fourteen-day follow-up rate (target above 60 per cent), and ninety-day funding velocity (target above 40 per cent for Series-A-targeted demo days). Track them cohort over cohort.

Should we run a demo day live, hybrid, or virtual? Live for the pitch block and the 1:1 window if at all possible: in-person follow-ups convert at higher rates. Virtual broadcast tracks are useful for international investors who cannot travel and for cohort transparency. Pure virtual demo days work for very small cohorts but lose the corridor-conversation value.