How to Prevent Investor Overload at Demo Days

The fastest way to ruin a demo day is to leave the distribution to chance. Open the matchmaking platform on a Monday morning, send the link to every fund on your list, and ten percent of the room ends up with ninety percent of the meeting requests. The top-tier partners delete most of them unread. The long-tail funds get nothing and quietly stop replying to next year’s invitation.

This is not a curation failure. The right investors are in the room. It is a distribution failure, and the only person who can fix it is the organiser. Founders cannot solve it from their side. Investors cannot solve it from theirs. The mechanics live in your platform settings, your invite calendar, and your matching rules.

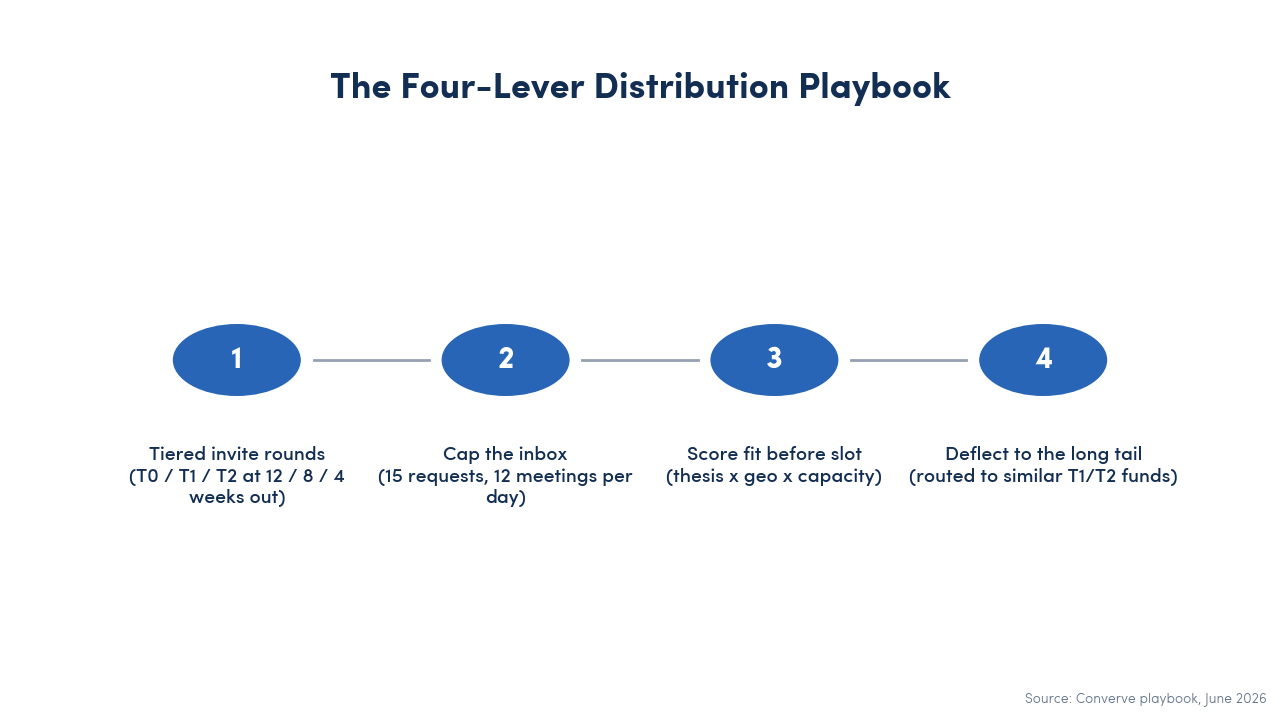

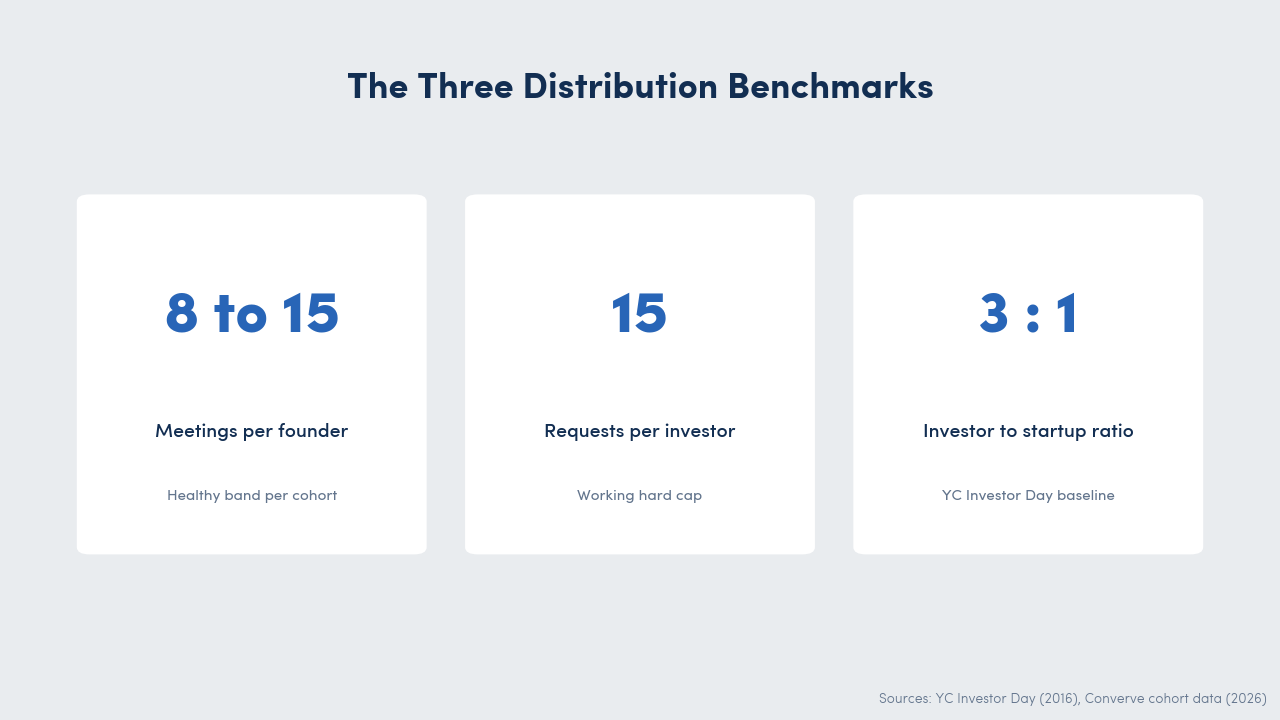

The short version: Investor overload at a demo day is a distribution problem, not a curation problem. Four organiser-side levers fix it: tiered invite rounds (T0, T1, T2), hard caps on requests and meetings, three-axis fit scoring before slot booking, and a deflection mechanism that redirects pitches from overloaded funds to a curated long tail. The healthy band stays the same in every cohort: eight to fifteen pre-booked meetings per founder, fifteen meeting requests as the working cap per investor profile.

Why Investor Overload Happens

The pattern is consistent across accelerator demo days, pitch competitions, and venture-firm showcases. Three causes do most of the damage.

The first is the flat invite list. Every fund on the spreadsheet receives the meeting platform link in the same email, on the same day. Top-brand partners are already overbooked by the time mid-tier funds notice the invitation in their inbox. The platform opens on a level playing field for thirty seconds and then collapses into a queue.

The second is the uncapped request system. Without explicit limits, every founder sends requests to the same fifteen brand-name partners. The top of the list looks like a denial-of-service attack. The bottom of the list sees a quiet inbox and assumes the platform is broken.

The third is single-axis matching. Most platforms treat thesis fit as a binary filter and ignore capacity. A Series A fund is technically a “match” for a pre-seed cohort because the sector tag matches, but the capacity for early-stage tickets is zero. The slot gets booked anyway. Two people waste a thirty-minute window neither of them wanted.

The cost is not theoretical. Y Combinator funnels roughly 196 startups onto a single stage in front of about 1,500 invited investors in its current cohort, and the post-event scramble is real enough that YC built a custom matching algorithm a decade ago to absorb it. Slush 2025 produced more than 20,000 one-to-one meetings in two days at a one-VC-to-two-founder ratio precisely because the matchmaking layer was engineered to distribute. Bits & Pretzels in Munich brings 1,500 investors representing €390 bn in assets under management into one hall, and the only way that does not collapse is structured distribution.

The Four-Lever Distribution Playbook

Each lever sits in a different place of the timeline. Run them in order and the demo day arrives with the room already balanced.

1. Tiered Invite Rounds: T0, T1, T2

Stop sending one invite list. Split your invited investors into three waves.

T0 is your anchor cohort. Five to ten lead-stage funds that match the cohort thesis exactly. They receive the invitation twelve weeks before the demo day, together with a private cohort briefing: anonymised sector breakdown, stage distribution, ticket-size signals. They commit to slots first, and their attendance becomes a quiet recruitment signal for the rest of the room.

T1 is your thesis-fit ring. Twenty to forty funds whose published thesis overlaps with the cohort sectors and stages. They receive the invitation eight weeks before the event. By the time they open the matchmaking platform, the T0 anchors are visible on the attendance list, which removes the “is this worth my time” question that kills mid-tier RSVPs.

T2 is your long tail. Corporate venture arms, family offices, regional funds, angel syndicates. They receive the invitation four weeks before the event. Crucially, T2 funds are not “leftover” investors. They are selected against an explicit thesis fit too, just with a wider sector aperture. The four-week lead time means they walk in with realistic expectations of which meeting requests they will get.

The result is a room that fills from the centre outward rather than from the loudest corner inward.

2. Cap the Inbox, Cap the Calendar

Two caps, both visible to founders inside the platform.

The first is a hard cap on incoming meeting requests per investor profile. Fifteen is the working number. It comes out of Y Combinator’s Investor Day mechanics, where the matching algorithm produced an average of 5.18 meetings per investor with a maximum of fifteen and a median of four. Above fifteen requests, the top of the funnel collapses into noise. Founders have to prioritise, which is the point.

The second is a soft cap on completed meetings per investor per day. Twelve is the working number on a single-day demo day, eight to ten on a two-day format. The literature on investor cognitive load is clear: after roughly a dozen pitches, partners stop remembering individual founders and start pattern-matching at the cohort level, which is exactly what you do not want.

For founders, the corresponding healthy band is eight to fifteen pre-booked meetings per person. Below eight, the cohort almost always under-delivers on funding. Above twenty, founders cannot follow up properly and the quality of every conversation drops. Track this metric cohort over cohort and you will see the funding outcomes track with it.

3. Score Fit Before Slot Fit

Replace single-axis matching with a three-axis scoring matrix that runs before any slot is booked.

The three axes are thesis fit (does the fund actually invest in this sector and stage), geographic fit (does the fund operate in the cohort’s market, or have a partner who does), and capacity fit (is the partner available, is the founder available, is the ticket range realistic). Only a triple match gets automatically slotted into the calendar. Single-match and double-match requests go into a wait list that the organiser releases manually as the room fills.

The point is not to make matching harder. It is to make the explanation visible. When a meeting is throttled or deflected, the organiser can show the founder which axis missed and offer an alternative. That is the difference between a platform that founders trust and one they route around in WhatsApp.

This is the operational layer where a structured founder-VC matching framework stops being theory and starts being calendar entries.

4. Activate the Long Tail Through Deflection

When a top-tier fund hits its cap, the request should not be lost. It should be deflected to a curated alternative.

Build a deflection table in advance. For each T0 anchor fund, list two or three T1 or T2 funds with a similar sector focus and ticket range. When a founder requests a capped T0 partner, the platform proposes the deflection target in the same flow: “Partner X is at capacity. Partner Y at Fund Z has a similar thesis and is open.” The founder can accept, modify, or decline. Either way, the request becomes a warm lead for the long-tail fund rather than disappearing into the queue.

The economic effect on next year’s invitation list is the part most organisers underestimate. Funds that receive deflected meetings come back. Funds that receive nothing do not.

Solution: Converve’s matchmaking layer is built around a meeting-matrix logic that is rule-based and audit-able, rather than a black-box recommender. For demo day organisers, that means every cap, every tier, every thesis-fit filter is explicit and reviewable before the platform opens to founders. When a request is throttled or deflected, the organiser can see why and override if needed. Talk to our team to see how the four levers run on a single platform.

The Numbers That Tell You It Is Working

The distribution playbook either shows up in the data or it does not. Track three numbers cohort over cohort, and your room will tell you whether the levers are tuned.

The first is the spread of meeting requests across investor profiles. A healthy cohort has a long-tail curve, not a hockey stick. If your top five investors receive more than forty per cent of all requests, your caps are too soft or your tiered invite waves are not staggered far enough apart. If the bottom quartile of investors receives no requests at all, your three-axis scoring is treating them as second class even though they are paying to be in the room.

The second is the deflection acceptance rate. Founders who accept deflected matches above sixty per cent of the time are signalling that the alternative recommendations are credible. Below forty per cent and the deflection table is wrong, usually because thesis sectors are too broad or ticket ranges are off.

The third is the long-tail return rate, the percentage of T2 funds that accept next year’s invitation. This is the slowest signal but the most consequential. A demo day that builds its long-tail return rate above seventy per cent is a demo day that has solved distribution as a structural problem, not a year-by-year scramble.

For the underlying cohort metrics, the six-phase demo day playbook covers the meetings-per-founder and follow-up KPIs that sit alongside these distribution numbers.

When the Playbook Breaks

Three failure modes show up reliably enough to plan for.

The first is when the T0 anchors do not commit. If five anchor funds drop out two weeks before the event, the entire wave structure collapses. The mitigation is to over-invite at T0 by a factor of one and a half and treat early commitments as a confirmation milestone rather than an assumption.

The second is when the cohort tilts. A demo day briefed as Series A turns out to be predominantly pre-seed because three traction-heavy founders dropped, and now the T0 cohort is wrong for the cap table. The mitigation is a short re-screen window in the last fortnight, where the organiser can swap in additional pre-seed funds and notify the affected T0 attendees with an honest update.

The third is when the platform settings get overridden under pressure. Senior founders who want unlimited requests, top partners who want their cap raised, sponsors who want their fund prioritised regardless of fit. The mitigation is to write the caps into the published rules and refer back to them. Once the rules become negotiable, the distribution collapses to whoever shouts loudest, which is precisely the situation the playbook exists to prevent.

Frequently Asked Questions

Why do investors get overloaded at demo days?

Because the matchmaking platform opens to all investors at the same time, with no cap on incoming requests, and most founders prioritise the same fifteen brand-name partners. The top of the room receives requests it cannot process while the long tail receives almost none. The cause is distribution mechanics, not the size of the cohort.

How many meeting requests should a demo day organiser allow per investor?

Fifteen is the working hard cap, in line with the YC Investor Day algorithm that produced an average of 5.18 meetings per investor and a maximum of fifteen meetings per startup at a roughly three-to-one investor-to-startup ratio. Above fifteen, the request signal becomes noise.

What is a tiered invite round?

A staged invitation system that releases the matchmaking platform link to three waves of investors at twelve weeks, eight weeks, and four weeks before the event. T0 is the anchor cohort of lead-stage funds, T1 is the thesis-fit ring, T2 is the curated long tail. The waves let the room fill from the centre outward.

How do organisers protect long-tail investors from being starved of deal flow?

By building a deflection table in advance. When a top-tier fund hits its cap, the request is automatically proposed to a similar T1 or T2 fund with the same sector focus and ticket range. Founders accept, modify, or decline. The long-tail fund receives a warm lead, the founder receives a meeting, the platform stays balanced.

What is the difference between thesis fit and capacity fit?

Thesis fit asks whether the fund invests in this sector and stage. Capacity fit asks whether the partner is available, the founder is available, and the ticket range is realistic. Most platforms score only the first axis, which is why a Series A fund ends up booked into a pre-seed cohort even though the capacity is zero.

Run the Levers Before the Platform Opens

The four levers are not new in isolation. Caps exist. Invite waves exist. Thesis scoring exists. Deflection exists. What is missing in most demo days is the discipline to set all four before the platform opens to founders, and then leave them alone once the wave starts.

The reward is a room where every investor has a calendar that justifies the trip, every founder has a meeting list that justifies the rehearsal, and the long-tail funds say yes to next year’s invitation. That is the version of a demo day that pays for itself in cohort funding velocity, not in stage applause.

If you are designing your next demo day and want to see the four levers running on a single platform, talk to our team about Converve. We will walk through tier setup, cap configuration, scoring matrix, and deflection rules with your cohort numbers, and you can decide whether the playbook fits before any contract.